After a frantic February, investors probably expect March to stick to its saying: like a lion, like a lamb.

In fact, February turned out to be a scary year, with yields on benchmark securities, represented by the 10-year Treasury note TMUBMUSD10Y,

and the 30-year title TMUBMUSD10Y,

recording its biggest monthly increases since 2016, according to Dow Jones Market Data.

The move was a strong reminder to investors that the bonds, considered mundane and upright by some investors, can wreak havoc on the market in the same way.

A final wave of negotiations, about $ 2.5 billion in sales close to Friday’s close, created a major hurdle for actions in the closing minutes of the session and may imply that there may be more pockets of air ahead before the market will stabilize next week.

The Dow Jones Industrial Average DJIA,

and S&P 500 SPX index,

it barely remained above its 50-day moving averages at 30,863.07 and 3,808.40, respectively, at the close of Friday.

‘An associated 10-20% sale of US stocks would also focus minds. But before that, the pain that is currently being distributed to growth-oriented stock portfolios may worsen. ‘Citigroup Strategists

“The turmoil is probably not over,” wrote Independent market analyst Stephen Todd, who runs Todd Market Forecast, in a daily note.

Even so, despite all the complaints about higher-than-expected yields, stocks in February still managed to achieve solid returns. For the month, the Dow ended up 3.2% higher, the S&P 500 recorded a 2.6% gain in February, while the Nasdaq returned 0.9%, despite a weekly loss of 4.9 % on Friday, which marked the worst weekly skid since October .30.

Many argued that a sale on the high-tech Nasdaq Composite was inevitable, especially with bustling stocks like Tesla Inc. TSLA,

just getting foamier in some measures.

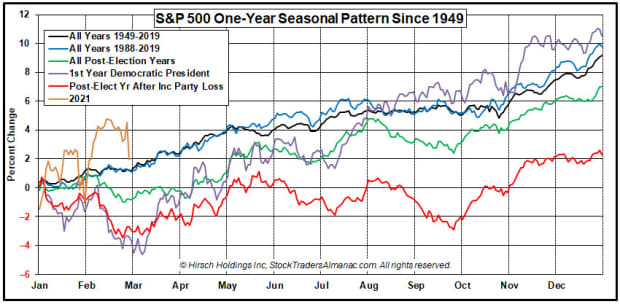

“But the market was overbought and extended throughout the year and possibly for several months in late 2020,” wrote Jeff Hirsch, editor of Stock Trader’s Almanac, in a note dated Thursday.

“After the big run in the first half of February, people are looking for an excuse to make profits,” he wrote, describing February as the weakest link in what is usually the best six-month earnings period for the stock market.

The beneficiaries of the recent movement in yields so far appear to be banks, which are benefiting from a steeper yield curve as long-term Treasury yields increase, and the financial sector S&P 500 SP500.40,

XLF,

ended with a drop of 0.4%, which is, apparently, the second best weekly performance of the 11 sectors of the index, behind the energy SP500.10,

which rose 4.3%.

Utilities SP500.55,

had the worst performance, down 5.1% on the week and consumer discretionary SP500.25,

it was the second worst, with 4.9%.

In February, energy registered a gain of 21.5% with the rise in crude oil prices, while finances rose 11.4% in the month, registering the best and the second best monthly performance.

So, what’s in store for March?

“Typical March trades come in like a lion and come out like a strong lamb during the first few days of trading, followed by hectic trades to decline until mid-month, when the market tends to rebound upwards,” writes Hirsch.

March also sees “triple witchcraft: occurs on the third Friday, when stock options, stock index futures and stock index options contracts expire simultaneously.

Ultimately, seasonal trends suggest that March will be unstable and can be used as an excuse for new sales, but in this slowdown it could be cathartic and make room for new gains in the spring.

“It is likely that there will be more consolidation in March, but we expect the market to find support soon and, later, to challenge the recent highs again,” writes Hirsch, noting that April is statistically the best month of the year.

Stock Broker’s Almanac

Looking beyond seasonal trends, it is not certain how the increase in bond yields will develop and, ultimately, spread across markets.

On Friday, the 10-year benchmark closed with a yield of 1.459% based on 3 pm Eastern closing, and reached an intraday peak of 1.558%, according to data from FactSet. The dividend yield for the S&P 500 companies in the aggregate was 1.5%, compared, while the Dow is 2% and for the Nasdaq Composite it is 0.7%.

As to the question of whether the rise in yields will pose a problem for stocks, Citigroup strategists argue that yields are likely to continue to rise, but the advance will be controlled by the Federal Reserve at some point.

“The Fed is unlikely to let real US yields rise well above 0%, given the high levels of public and private sector leverage,” analysts at Citi’s global strategy team wrote in a note dated Friday entitled “Rising Real Rising: What to do. “

Adjusted real yields are usually associated with inflation-protected Treasury bond rates, or TIPS, which compensate investors based on inflation expectations.

Actual yields have been negative, which undoubtedly encourages risk taking, but the launch of the coronavirus vaccine, with a Food and Drug Administration panel on Friday recommending Johnson & Johnson’s JNJ approval,

the one-jab vaccine and the prospects for more COVID aid from Congress are increasing the prospects for inflation.

Citi notes that 10-year TIPS yields have fallen below minus 1%, with the Fed’s quantitative easing last year to help ease the stress in the financial markets created by the pandemic, but in recent weeks, strategists have noted that TIPs rose to minus 0.6%.

Reading: Here’s what a hedge fund trader says happened in Thursday’s bond market rage, which sent the 10-year Treasury yield to 1.60%

Citi speculates that the Fed may not intervene to contain market disruptions until investors see more pain, with the 10-year term reaching 2% before the alarm goes off, which would bring real yields close to 0%.

“An associated sale of 10-20% in US stocks would also focus on minds. But before that, the pain that is currently being distributed to growth-minded equity portfolios may worsen, ”wrote Citi analysts.

Output check: Cracks in this multi-decade relationship between stocks and bonds can cloud Wall Street

Damn!

Analysts do not appear to be taking a bearish stance per se, but warn that a return on returns that is closer to normal historically can be painful for investors heavily invested in growth stock names compared to assets, including energy and finance, which are considered worthwhile investments.

In the meantime, markets will seek more clarity about the health of the labor market next Friday, when February’s non-farm payroll data is released. A big question about this key indicator of employment health in the US, in addition to how the market will react to the good news in the face of rising incomes, is the impact that the colder than normal February climate has on the data.

In addition to employment data, investors will be on the lookout for February manufacturing reports from the Institute for Supply Management and construction spending on Monday. Service sector data for the month is due on Wednesday, along with a private sector payroll report for Automatic Data Processing.

Reading: The current liquidation of the bond market is worse than ‘taper tantrum’ in an important way, argues analyst

Read too: 3 reasons why rising bond yields are gaining momentum and shaking the stock market